|

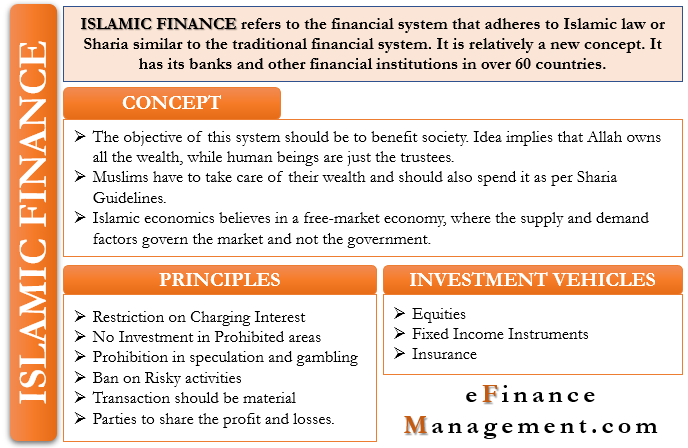

Get a cash lump sum of $2,000+ for refinancing to a low-rate loan. Islamic home loans come with many of the features that are also offered with traditional home loans. Compare the features among different lenders before deciding which home loan is right for you. And of course, this opportunity is not limited to domestic Australian markets. Leading Australian firms will Islamic Finance Australia seek out opportunities to become involved in offering Islamic finance products in the global market so they can tap alternative funding sources and invest in new areas. On 13 October 2010, the Board of Taxation released itsdiscussion paper on the reviewof the taxation treatment of Islamic finance, banking and insurance products. The Chairman of the Board of Taxation announced the release of the discussion paper viaa press release. The Board has developed this discussion paper to facilitate stakeholder consultation. On 3 May 2016, the Government announced the release of the Board’sfinal reporton the taxation treatment of Islamic finance, banking and insurance products. Even during these challenging times their team are willing to help. We have now provided more than $300 million of Islamic finance to customers nationally and our presence has grown across Australia with representatives in each state. Our Low Doc products may be the perfect solution for self-employed business owners who do not have the standard financials. This authorisation allows us to offer banking services, but is subject to certain restrictions such as a cap on the amount of deposits that we can hold in total. The purpose of the “restricted” status is that we can test our systems and processes before launching as a fully unrestricted bank. Put simply, it is the application of faith-based norms and principles derived from shariah dealing with financial transactions and trade practices. It relies on rules and injunctions developed from Islamic jurisprudence. They deal with the lawful and the prohibited , ethical conduct, contracts and obligations. Another financing company, Hejaz Financial Services, which is already in the home loan and superannuation space, says it has also just started the process of applying for a R-ADI.

“There are developers that we work with that in the past just haven’t used any bank finance so we deliver projects with 100 per cent of their own equity,” said managing director Amen Zoabi. “Interest-free banking was non-existent in Australia, but it did exist in Canada where I had previously been studying,” he said. When Professor Ishaq Bhatti came to Australia 30 years ago, the bank teller looked bemused when he asked for a savings account that didn’t accrue interest. Under Islamic law, or Sharia, there is a prohibition Sharia Home Loans Australia on charging or paying interest, which is called riba and considered exploitative because the lender does not assume a share of the risk. That said, after several years of working with scholars, Australia lawyers, regulators and suitable funding sources, we opened our doors to the public with our Islamic finance solutions in 2015. How ICFAL gives you the chance to Shariah Compliant investment and financing. The global coronavirus pandemic may be causing a lot of anxiety and stress for people across Australia. Marking 25 years in operation, we are excited to share our brand new visual identity. An identity that captures and expresses our values, product, and promise to a better community. Make sure you have a clear understanding of exactly how much extra you’re being charged as a result of the profit rate. Murphy stresses that when comparing Islamic home loans, you should keep an eye out for the service level offered by the provider. The fundamental difference between a typical home loan and a Sharia-compliant home loan is in the borrowing terms used (i.e. interest with a typical home loan vs rental or profit fee with an Islamic home loan). For the period of the transaction, the buyer amortised the outstanding debt through rental instalments. APRA has granted a restricted banking licence to Australia’s first Islamic bank, which plans to offer home finance through the broker channel. While the bottom line is important, in a world where corporate governance and social impact adds to brand gravity, ethical consciousness must take precedence when developing products and services. We offer an alternative solution for Muslims in an Australian landscape. With the number of Muslims in Australia growing by more than 6 per cent every year, we’re excited to be bringing this new type of banking to the Australian community,” the CEO added. Similarly, for personal finance – Islamic Bank Australia would purchase the item and then sell it to the customer. Interest-based home loans that dominate our market generally allow people to borrow money from a bank, buy a house with that cash, and then pay the money back over a fixed term to the financier with interest. After a successful pre-assessment a finance executive will prepare your application for submission. Islamic Car Finance Australia The information we request will vary depending on your personal circumstances and includes documents to support income, deposit or equity, assets, liabilities such as current mortgages, car loans, credit cards etc. In establishing Amanah our objective was to address the absence of a Shariah compliant home financing solution that met the standards of globally recognised Shariah scholars whilst also complying with Australian laws and credit regulations. Ijarah Finance was established to help you purchase a property without entering into an interest-based mortgage. APRA grants restricted ADI licence Halal Car Finance to Australias first Islamic bank Please be aware that this might heavily reduce the functionality and appearance of our site. It’s a totally new way to think about banking,” said Mr Gillespie. Islamic finance is based on a belief that money should not have any value itself, with transactions within an Islamic banking system needing to be compliant with shariah . The rise of Islamic banking is just the beginning of a much larger discussion around ethical banking and financial inclusion, one which banks have struggled to stay on top of for years, if not decades to now. The challenge lies in keeping up with the pace that society is changing — and technology is at the forefront for influencing those societal changes. There is still a lack of information about financial exclusion according to ethnicity or religious group in Australia. The Muslims communities are financial excluded mainly due to their faith and religious beliefs, because Islam prohibits Riba which is widely practiced in conventional banking and finance operations. The level of awareness about the Islamic finance products and services in Australia is still limited. Also the lack of Islamic financial products and services is a contributory factor of financial exclusion. The introduction and wide spread offer of Shariah-compliant financial products and services by Islamic and conventional financial institutions can increase nationwide financial inclusion. Some argue that Islamic finance simply interchanges terminology and concepts and that Sharia-compliant home loans don’t differ greatly from standard home loans. Home loan applications continue to decline, according to the latest Equifax data. Without this approach, the gap on financial inclusion will only widen or contribute to diminishing financial health. IBA's licence is timely too, with the 2021 Australian Census highlighting a 34.6 per cent increase in Australia’s Islamic population — now the second largest religion in our country. We update our data regularly, but information can change between updates. Confirm details with the provider you're interested in before making a decision. With an Islamic home loan, you can choose the home and then the financial institution will buy it from the seller. This same financial institution then agrees to lease the home for a pre-determined period, which is known as Ijarah Muntahiyah Bittamlik. At the time of the final lease payment, ownership of the home will be transferred to you in the form of a promissory gift or hiba. The Board requested written submissions on the review of the taxation treatment of Islamic finance products by 17 December 2010. Copies of public submissions made to the Board are available below. Make recommendations and findings that will ensure, wherever possible, that Islamic financial products have parity of tax treatment with conventional products. Finder.com.au is one of Australia's leading comparison websites. We compare from a wide set of banks, insurers and product issuers. We value our editorial independence and follow editorial guidelines. This flexible variable rate home loan offer from a digital lender is suitable for both home buyers and investors. Are there any Sharia home loans or Islamic banks in Australia? Even with an Islamic mortgage, if you have less than a 20 per cent deposit, you’ll have to pay Lender’s Mortgage Insurance . Your lender owns the security over the property, so if you stop paying the mortgage, the lender can force the sale of the property to recoup the outstanding money. By sending a press release and/or signing up for a subscription of our service Get The Word Out, you agree to the following terms of use, limitations, quality policy and fair use policy. The typical Australian home loan earns a certain amount of interest annually. That interest is the profit the financial institution makes when you borrow its money. Sharia Law offers Muslims a broad set of rules for living an ethical life.

A lot of it comes with just educating the customers of what Islamic finance is, he says. "You have to remember it is a business at the end of the day, it's not a charity," he says. "But it's a more ethically, morally-based banking than just interest-based, where it's just greed. Islamic banking has certain religious values and guidelines." We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. As the mortgage term progresses, the homebuyer gains more and more equity in the property and owes less interest. At the end of the mortgage, the homebuyer owns 100% of their home, and the lender’s involvement is over. We are licensed to advice on any financial products in Australia and are Sharia certified by an internationally acclaimed authority. Binah who specialise in delivering full scale construction services have utilised NAB’s new Islamic financing product on their latest development. Would you really like to own your own home, but find it a struggle to save up the whole cost of a suitable property? If you’d ideally like a home loan but are worried about it contravening Sharia law, take heart. There is a misconception amongst the general public that Islamic finance is the same as conventional, simply because both specify the finance cost as a percentage. This is a huge misnomer because using a percentage is just a method of pricing. Hence, what is most important is not the use of the percentage, but rather what such a percentage represents. Consider whether this advice is right for you, having regard to your own objectives, financial situation and needs. You may need financial advice from a suitably qualified adviser. For more information, read Canstar’s Financial Services and Credit Guide and our detailed disclosure. Canstar may receive a fee for referring you to a product provider – for further information, see how we get paid. Various forms of Islamic home financing are offered by a handful of service providers in Australia. This combination of rental and sale contract makes it the best halal financing product for property ownership while you get to own the house of your dreams and call it home. The Australian Financial Review Dr. Kabir Hasan said that conventional banks will give you loans, and they will charge interest in return, this is how ordinary banking works. To meet with Islamic law requirements, finance needs to be structured as a lease where rent and service fees are paid instead of interest or some other kind of profit-sharing arrangement. Muslims can participate in similar investment vehicles and money transfers as non-Muslims. Islamic banks help people of all backgrounds manage their money. You can also contact other banks to find out if they offer Islamic home loan options. Keri is a financial services professional with significant experience in investment sales and marketing, strategy and management, superannuation and business consulting and governance, and an experienced company director. Melbourne-based investment advisory firm Hejaz Financial Services has also applied for a banking licence after seeing huge demand for its sharia-compliant finance, mortgages and superannuation since 2013. Commission share on referrals to third party advice providers (mortgage/finance/insurance broker, financial adviser, financial institution, utilities provider or any other third party). Income could be an upfront commission and/or ongoing commission. The commission depends on the amount of the finance, cost of the product or other factors and may vary from product to product. The new Islamic banking technology prototype will allow Australian financial institutions to plug in and provide personalised Islamic services to their customers, across savings and transactions accounts, and lending. The salient benefit of an Islamic finance facility is that there is an ethical overlay applied to it, whereby both loan funding and loan purpose have an ethical requirement. Moreover, the mortgage products can be highly competitive with rates offered by many conventional non-bank lenders, and in some cases, may be cheaper than those offered by non-Islamic lenders. Secure the future of your children by investing for a tomorrow they truly deserve. Invest ethically and get Shariah compliant returns as you move one step closer to your goals. Money is a big deal for everyone so we’re here as your money partners, finding the best way to make it happen. Finally, Shariah-compliant home financing is now available. A seminal book on Islamic finance by the world-renowned Mufti Taqi Usmani, this is a must-read for anyone interested in the key concepts, rules, and ideas behind modern Islamic finance. A brief, useful guide to the principles of Islamic Finance, delivered by an Australia-based authority in the field, Almir Colan. Consider whether this advice is right for you, having regard to your own objectives, financial situation and needs. You may need financial advice from a suitably qualified adviser. For more information, read Canstar’s Financial Services and Credit Guide and our detailed disclosure. Islamic Finance Halal Loans Sharia Finance Australia The Islamic Finance News awards honour the best in the Islamic finance industry and are one of the most prestigious awards highly recognised by global Islamic finance capital markets. We have now provided more than $300 million of Islamic finance to customers nationally and our presence has grown across Australia with representatives in each state. If you're buying your first home, an investment property or if you want to change your current home loan to a Shariah compliant option we can help. Our experienced consultants can help your business reach new heights by offering Ijarah lease agreements to enable your business to acquire or lease assets such as motor vehicles, trucks, plant equipment, machinery & more. Our Low Doc products may be the perfect solution for self-employed business owners who do not have the standard financials. Find out the latest insights about super, finance and investments. “Financial advisers need to be more cognisant, ask the right questions, and service the unique needs of their individual customers,” Mr Ozyon said. Pointing to this lack of financial literacy, Mr Ozyon argued that there is a clear appetite in Islamic community for proactive financial management advice. Hejaz Financial Services is looking to capitalise on that opportunity. The company is currently in the process of applying for a restricted ADI licence with the Australian Prudential Regulation Authority. “It’s almost 2022 – Muslims shouldn’t have to stuff money in their mattresses, forego interest on their superannuation or struggle to save enough cash to purchase a home outright like I had to,” he said. Finder acknowledges Aboriginal and Torres Strait Islanders as the traditional custodians of country throughout Australia and their continuing connection to land, waters and community. If you need to explore your options, you may want to speak to a mortgage broker. They have the necessary knowledge and experience to help you find the best lender that meets your needs, preference, and budget. Get a cash lump sum of $2,000+ for refinancing to a low-rate loan. They were organised, very professional and have excellent customer services. I have been with Amanah since March 2019 and so far their service has been superb from the beginning. Even during these challenging times their team are willing to help. If you are going to make an offer at a private sale please ensure your lawyer requests Halal Loans a “subject to finance” period. Ultimately, we want to bring our Shariah compliant products to the grass roots of our community and we have leading representatives in each state that can assist you. We have been recognised for our commitment to client service having been awarded the Best Islamic Finance Institution for three consecutive years by the prestigious. That's no doubt helped push them along while some of the major banks, especially in the U.S., have collapsed or needed billions of dollars in government funds after taking on too many bad loans. Founded in 1989, MCCA is the first and one of the leading providers of Islamic finance in Australia, a small but growing market. There's little competition other than a few others such as Sydney-based Iskan Home Finance. Some time ago, Amanah Finance's Asad Ansari consulted for an offshore Islamic bank that was interested in setting up a branch in Australia. "I'm a Halal butcher, with a Halal investment, and a Halal superannuation." "I'm very grateful that this is allowing me to grow my business," he says. "A lot of people that we know that are Muslims have gone with conventional ways." This attracts double stamp duty too, and was one area looked at by the taxation review that Asad participated in. The complication in the Australian context is that laws aren't set up for this style of lending, so technically the home is owned by the household from the beginning, but with a legal agreement that the Islamic lender is entitled to it. He bought a three bedroom home in Campbellfield, outside of Melbourne, in December for $270,000, paying a 20% deposit. That part is not unlike anything other Australians would do in purchasing such a home. Perhaps the largest issue, however, is the fact many Australian Muslims, while growing in number, see the traditional lending method with banks here to be both easier and cheaper. One way to avoid any interest payments would be to pay entirely in cash for a property, but few could ever afford such a transaction in Australia. Another option would be to borrow from friends,

0 Comments

Leave a Reply. |

ArchivesCategories |

RSS Feed

RSS Feed